How to Compute for Salaries, Wages and Benefits Part 1

If you already have experienced working in a certain company or are presently working in one for more than a month, then you already know what a basic payslip is, which is equivalent to every worker’s bi-monthly wage.

If you have not, then this computation shows you how a basic payslip should looked like before you receive them twice a month. Do note, however, that the way your wage is computed may not necessarily reflect on your actual payslip.

Formula:

Taxable Income = (Monthly Basic Pay + Overtime Pay + Holiday Pay + Night Differential) – (SSS/PHILHEALTH/PAG-IBIG deductions – Tardiness – Absences)

Net Pay = Taxable income – Withholding Tax

Definition of terms

Monthly Basic Pay:

The agreed upon monthly pay you get for working in a company whose amount varies depending on the agreement. Since workers in the Philippine setting are paid in a bi-monthly basis (twice a month), your basic rate for either half can be gotten by dividing your monthly basic pay by two.

Overtime Pay:

The pay you receive in addition to your monthly wage as a result of an overtime work (how to compute for Overtime pay)

Holiday Pay:

An added pay to your monthly wage resulting from working during a holiday event (how to compute for holiday pay)

Night Differential:

A higher-than-day-counterpart daily rate pay, commonly higher by 10% (how to compute for night shift differential)

Deductions:

SSS (please refer to SSS Contribution table)

PHILHEALTH (please refer to PHILHEALTH Contribution Table)

PAG-IBIG: 2% from the employee’s monthly basic pay or 100 pesos whichever is lower

Tardiness:

A deduction to the monthly wage as a result of the failure to report of an employee to his assigned role and act on it on time

Absences: A deduction equal to the number of days away from work

Say, for simplicity’s sake, we have a minimum wage earner of 12,000 pesos working in a province on a dayshift basis but never worked past 5 PM in a 8 AM to 5 PM schedule nor did he work during any of the possible holiday event on that particular month and only pays contributions (SSS/PHILHEALTH/PAG-IBIG) at the bare minimum yet at the same time was never tardy nor ever absent throughout a month of working period, then we would only need the following values with the computation based on the formula:

Taxable Income = (12,000 + 0 + 0 + 0) – (120 + 137.50 + 100 – 0 – 0)

= 12,000 – 357.5

= 11,642.5

However, computing for the taxable income does not give you the full figure of what you’re going to get with your monthly wage. The government, after all, cannot live without its lifeblood – taxes. Employers are required to withhold this from the employees’ wages. This is called the withholding tax.

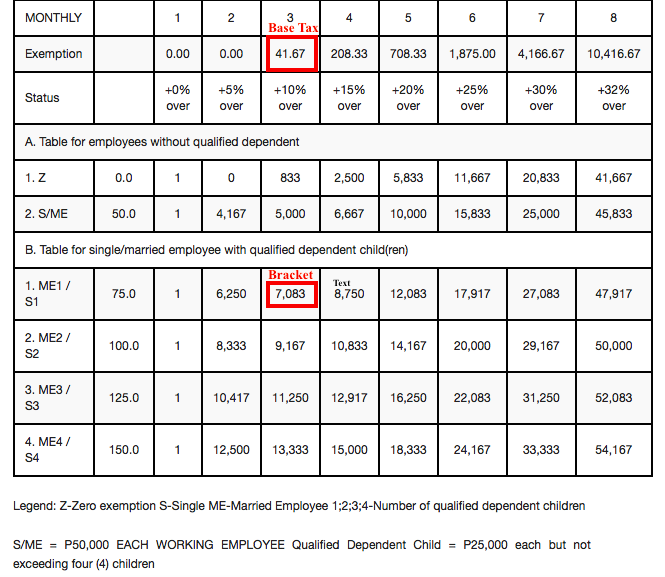

To compute for the withholding tax, let’s refer to the Bureau Internal Revenue’s own withholding tax table for reference on its computation.

Using the table as the reference with the same person as the sample as before, let us add the following information in the equation to get a perfect sense of what a withholding tax is in relation to your monthly basic pay:

Tax Schedule: Monthly

Status: ME1

Bracket or Exemption: 7,083

% Over: 10%

Base Tax: 41.67

source: http://www.bir.gov.ph/index.php/tax-information/withholding-tax.html]

Using the formula:

Withholding Tax = [(Taxable Income – Bracket or Exemption) * (% Over)] + Bracket Tax or Base Tax

= [(11,642.5 – 7,083)] * 10% + 41.67

= [(4559) * 10%] + 41.67

= 455.9 + 41.67

= 497.57

Deducting the withholding tax with your taxable income, then you will be getting a computation for your month-long work pay.

Net Pay = 11,642.5 – 497.57

= 11, 144.93

Need help on computation of your employees’ salaries? For , ask our friendly accountant.